To Desktop or Not to Desktop? That is The Question

Fannie Mae and Freddie Mac both announced earlier this year the implementation of the use of Desktop Appraisals beginning in March. There has been much discussion and questions regarding these products so I thought I would share some information and thoughts on the topic.

Why would the GSEs want this product?

- Appraisal Modernization- Many in the industry are trying to move the appraisal industry to modernize with the use of technology and data gathering services. If anyone has been in the appraisal industry for a while they do know that it has been changing with technology. Appraisers no longer use typewriters, fax machines, or one-hour photo labs. As technology has evolved we have much greater access to data and appraisers are learning to adapt and use this technology. Many believe that the use of different data gathering tools and sources will help modernize the appraisal process.

- Covid19 Response- As the pandemic hit, the GSEs implemented the Covid Flexibities that appraisers could perform desktop appraisals so that they would not have to go into the homes for the safety of the homeowners and appraisers. The appraisers were able to perform these appraisals using photos either provided by the homeowner or from recent photos available on the MLS. If the appraiser was confident that the data was reliable, they would complete the appraisal as a desktop using the Covid Flexibilities, which had a different scope of work and certifications. The GSEs determined that these products were good and have decided to make them a permanent option.

- Efficiency- as the recent spike in the demand for appraisal services peaked and there seemed to be a bottleneck in the time to get appraisals completed. This process is seen by some to be a time saver as the appraiser would no longer have to spend the time driving to the property and taking comparable photos.

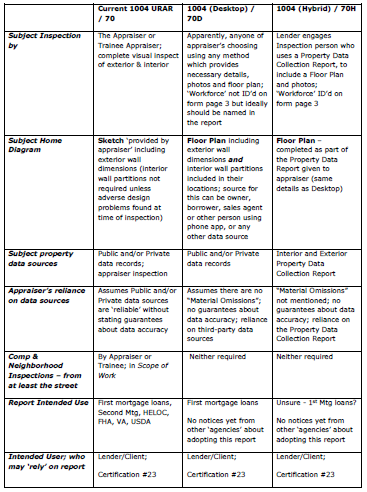

Differences in Appraisal Products

There are many different types of appraisals, a full appraisal, a drive-by appraisal, desktop appraisals, and hybrids. Many have been confused about the differences between Desktop Appraisals and Hybrid Appraisals.

It is my understanding that the Hybrid Appraisals use data provided by third parties and that for the Desktop appraisals the appraiser determines if there is enough data available from reliable sources to perform the appraisal. The appraiser may be able to use remote tools to view or sketch the property. Both Desktop and Hybrid appraisals require a floorplan rather than a traditional sketch from the appraiser. Here is a good reference from FNMA & Freddie Mac: URAR Hybrid and Desktop Appraisal Forms

Dave Towne, Certified Residential Real Estate Appraiser; owner of Appraiser Education Service, recently wrote an article published in Working RE that discusses some of the differences between the Full, Desktop, and Hybrids as well as questions around them.

Tools for Desktops/Hybrids

Some of the current new tools and technology that I am aware of that assist with Desktops and Hybrids are:

RemoteVal- This tool is a free app from Incenter that allows the appraiser and homeowner to inspect, view, measure, and take pictures of a property remotely.

Cubicasa– Allows appraisers or trainees or third parties to sketch a floor plan of a house using technology from a phone or tablet.

INvision Capture– This tool from Class Valuation provides a floor plan and sketch to ANSI standards.

Homeview Inspection Tool- This tool from Valuelink provides an inspection tool to view a property and take photos.

InsideMaps– A tool that provides mapping, sketches, and tours of homes. This tool is not free and pricing is based on the size of the home.

These are just a few that I am aware of and I am sure that the technology will improve and other companies may provide these tools if there is a demand.

Not All Properties Qualify

It is important to note that these desktops will not be available for every property. Per FNMA Selling Guide:

Eligible Transactions

To be eligible for a desktop appraisal, transactions must meet the following criteria:

- one-unit property (including those with an ADU and units in a PUD),

- principal residence,

- purchase transaction (including new construction),

- LTV ratio less than or equal to 90%, and

- DU loan casefile that receives an Approve/Eligible recommendation.

Ineligible Transactions

The following transactions are not eligible for a desktop appraisal:

- two- to four-unit properties;

- condo and co-op units;

- manufactured homes;

- construction-to-permanent loans (single-close and two-close);

- second homes and investment properties;

- all refinances;

- HomeReady, HomeStyle Renovation, and HomeStyle Energy loans;

- Community Seconds with a subsidized sales price;

- Community land trusts, or other properties with resale restrictions (loan casefiles using the Affordable LTV feature);

- DU loan casefiles that receive an Ineligible recommendation; and

- manually underwritten loans.

Acceptance of Desktops & Hybrids

Although the FNMA & FreddieMac have accepted these products there some questions many appraisers have.

- Concerns over the lack of a physical inspection– Many appraisers are concerned about the lack of a physical inspection. What about foul odors? Cracks in foundations or unstable floors when walking on them. Appraisers have been trained in knowing what to look for. If the property information is being provided from a third party are they trained? How can appraisers know that some of the areas of a property are not being shown?

- Concerns over liability– Appraisers are the ones signing the report. Many appraisers are not comfortable performing these assignments as they are the one that assumes the liability. Many are not confident knowing that the data provided such a condition or size of the property is accurate. Without confidence in the accuracy of the data, many appraisers will not choose to perform them.

- Concerns over fees & time- Many appraisers do not think that these products will save time. There will be additional time spent verifying the accuracy of the data provided. I know that for me personally, as more and more data has been made available to me on an assignment, the more discrepancies I find, therefore additional time is needed to confirm the accuracy. Many are thinking that fees will be too low for the additional liability and time needed.

What Do You Think?

This is a great time and opportunity for appraisers to weigh in on how they feel about these products. Will you do them? Why or why not? Here are a few surveys available that I am aware of. Please let me know if there are others.

Surveys:

Working RE: Desktop and Hybrid Appraisal Survey (surveymonkey.com)

Bradford Technologies: New GSE Desktop Appraisal Survey (surveymonkey.com)

To me, the verification of data is going to be essential to have confidence in the appraisal. The more data we get the more important the verification of the data becomes. It is my understanding that the appraiser will be assuming all liability. I already have a hard time reconciling discrepancies in data between CAD & CoreLogic/Realist data so additional time will be needed for this. I also foresee additional time with the tool where the appraiser guides the homeowner. It seems like too many things can be missed, such as foundation issues or smell. If a realtor or homeowner provides the data then that would not be an uninterested party.

At this time, the majority of our work is rural and complex and we don’t anticipate that these would qualify for this type of assignment. I do see that perhaps these might work if you were to take on a trainee and the trainee was able to do the inspection and use the tools for a floorplan. This solution might help appraisers’ liability concerns as they would trust someone that they trained and help incentivize appraisers to take on a trainee.

Informational Posts about Desktops & Hybrids

Policy Update- Desktops and ANSI Square Footage Calculation– Appraisal Institue

Desktop to Become the New Norm– Working RE Magazine

About Desktop Appraisals– Fannie Mae

A View on Risk- Desktop Appraisals– Appraisal Buzz

Desktop Appraisals- What are They and Will You Do Those Assignments? -Working RE Magazine

The Appraiser Trainee- The Solution that Has Been Avoided– Skap The Appraiser

About The Author

Shannon Slater

Shannon is a Certified Residential Real Estate Appraiser and serves as the Vice President of the DW Slater Company. She joined David at the DW Slater Company in 2006. Shannon graduated Cum Laude from the University of North Texas with a BA degree. Prior to joining the DW Slater Company, she was an Elementary School Teacher for the Pilot Point Independent School District. Shannon is an FHA Certified Appraiser. Shannon is a designated member of the National Association of Appraisers and a member of the Association of Texas Appraisers. In her free time, Shannon enjoys spending time with her family, singing in a local church choir, and tandem cycling with her husband.

Timely post. My work is similar to yours, mostly small acreage residential that does not lend itself well to desktop appraisals. My main concerns are not necessarily liability but in how to I maintain my income. I’m not interested at present because I expect to not save significant time doing this work plus I expect lenders to want a discount. If my normal work dries up I might reconsider but for now, I’m busy.

FYI-My appraiser association is putting together an intro to desktops class for early April with two very smart appraisers, one directly involved with desktops at an AMC and the other a top private party appraiser. CE will be only for California plus likely Nevada but the content should help all appraisers decide on whether to start this type of work and best practices if you do.

Thanks, Joe. Yes I hear so many things in different groups and there seems to be some confusion about them and uncertainty about the use of them. Did you fill out the surveys?

This was really comprehensive. I’m definitely going to link to your post whenever I decide to write something about this. Outstanding job.

Thanks, Ryan! I’ve been saving links and resources for myself and thought I would go ahead and share with others along with my thoughts. I hope you were able to do the surveys.

thanks. well written and comprehensive. i’ve shared with my staff.

Thank you for your input and for sharing

Great recap of what’s going on with desktops. At the current time, I am not interested in doing them as it will take just as much time or more to verify the information provided to make sure it is correct. I do believe there could be some liability issues if the information leads the appraiser to produce a report that is not credible.

Thanks Tom for your input and thoughts. I agree that additional time will be needed to verify the data. Accuracy if the data will be essential in being able to provide a credible report.

Very well said. To add, we also have concerns regarding data collectors being unregulated, unlicensed, untrained, uninsured and basically no assurance that the photos, videos, etc will be properly protected from wide dissemination. Also would homeowners want to take on the responsibility of videotaping their residence and belongings? So many questions and way too much liability. Advancements and change can be a good thing however this just makes no sense as it will not save time or money.

Thanks, Donna. Those are very legitimate concerns. Our background checks are there for a reason. This is something that definitely needs to be addressed.